Understanding Blockchain: How This Digital Ledger Transforms Industries

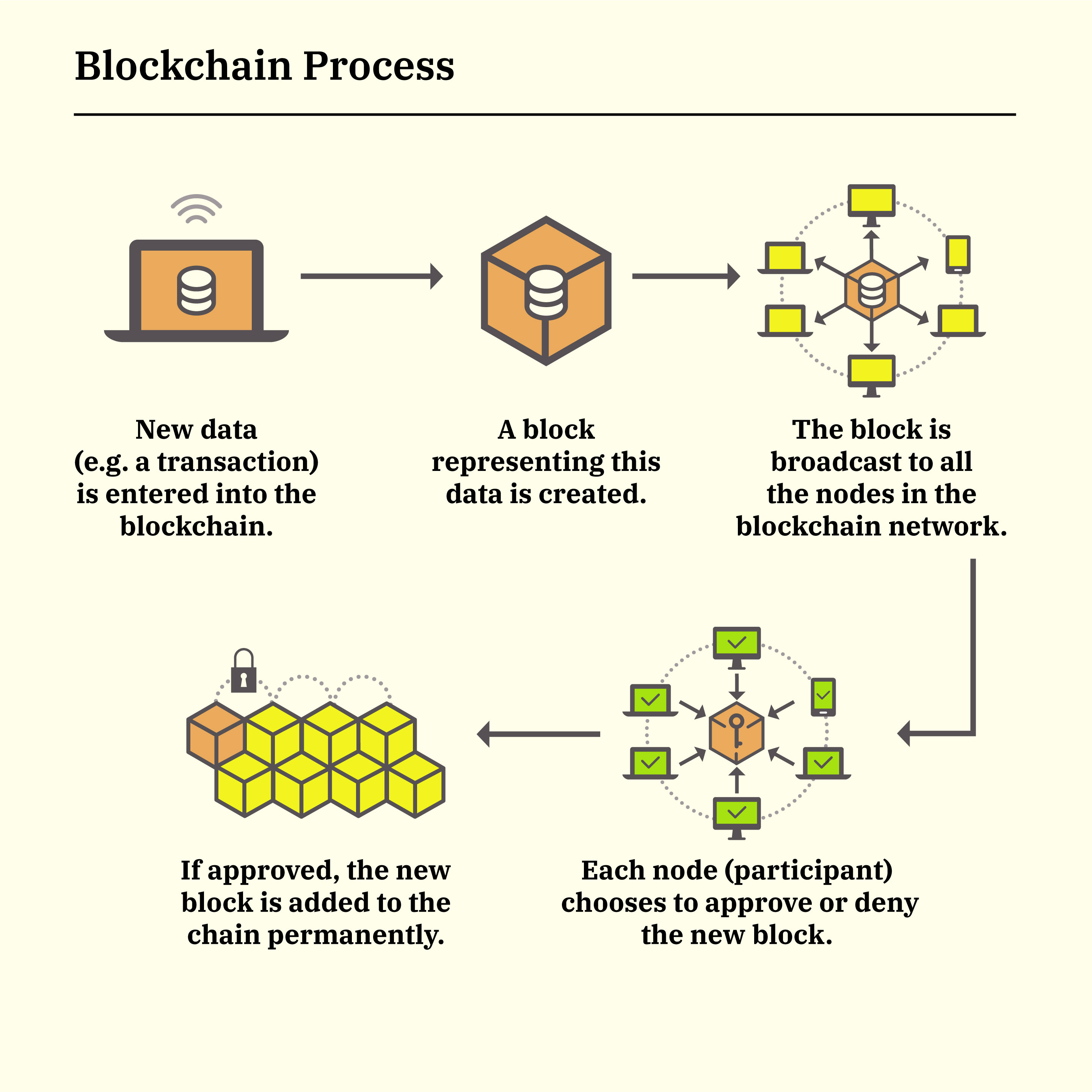

Blockchain is a revolutionary technology that serves as a digital ledger, enabling secure and transparent transactions. By decentralizing data storage, it eliminates the need for intermediaries, reducing costs and enhancing efficiency. This distributed ledger system records transactions across multiple computers, ensuring that the information is immutable and easily verifiable. Industries such as finance, supply chain, and healthcare are leveraging blockchain to streamline operations and increase trust among stakeholders. From enabling faster cross-border payments to providing end-to-end visibility in supply chains, the potential applications are vast and transformative.

Moreover, the impact of blockchain extends beyond just operational efficiency; it also fosters innovation in new business models. For example, the rise of decentralized finance (DeFi) platforms has challenged traditional banking systems by offering peer-to-peer lending and trading without intermediaries. Additionally, industries like real estate are utilizing blockchain to simplify property transactions, allowing for swift and secure transfers of ownership. As more sectors begin to understand and adopt this technology, blockchain is poised to reshape how we conduct business and interact with digital assets.

Blockchain Basics: What You Need to Know About the Future of Transactions

Blockchain technology is rapidly transforming the way we think about transactions across various industries. At its core, a blockchain is a decentralized digital ledger that records transactions across multiple computers, ensuring that the information is secure, transparent, and immutable. This innovative approach not only reduces the risk of fraud but also enhances efficiency by eliminating the need for intermediaries. As we delve into the future of transactions, understanding the foundations of blockchain is essential for anyone looking to navigate the evolving digital landscape.

One of the key benefits of blockchain technology is its ability to facilitate peer-to-peer transactions, allowing users to engage in commerce without relying on traditional financial institutions. This shift is particularly significant in regions with underdeveloped banking infrastructure. Moreover, the introduction of smart contracts – self-executing contracts with the terms of the agreement directly written into code – promises to streamline processes and reduce costs across various sectors. As we move forward, it's clear that embracing blockchain basics will be crucial for businesses and individuals alike, positioning them at the forefront of this digital revolution.

Is Blockchain the Solution to Data Security? Exploring Its Benefits and Challenges

Blockchain technology has emerged as a promising solution to the growing concerns surrounding data security. At its core, blockchain operates as a decentralized ledger that ensures data integrity through cryptographic principles. Unlike traditional databases that are susceptible to single points of failure, a blockchain distributes data across a network of computers, enhancing resilience against hacking and unauthorized access. Additionally, the transparent nature of blockchain allows for real-time monitoring and auditing, further bolstering trust among users and stakeholders.

However, despite its potential, the adoption of blockchain for data security is not without challenges. Issues such as scalability, regulatory compliance, and the energy consumption of certain blockchain protocols can hinder widespread implementation. Furthermore, the complexity of integrating blockchain into existing systems may require significant investment in time and resources. As organizations weigh the benefits against the challenges, it becomes crucial to carefully evaluate whether blockchain is the right fit for their data security needs, ensuring a balanced approach to leveraging this innovative technology.